WinCo Wins The Pricing Game In Eastern Washington/Northern Idaho’s Inland Valley

April 15, 2020 | 11 min to read

WALMART PRICING REPORT Round XXXII

Originally printed in the March 2020 issue of Produce Business.

With a rapidly growing population, consumers looking for low-priced produce will find it at only two of these seven stores studied.

Editor’s Note: We asked veteran retailer and Produce Business columnist Don Harris to visit each store to give his observations and opinions. Please see “Don’s Notes” in the boxes that follows.

This is the 32nd edition of the Produce Business Walmart Pricing Report. It was completed just before pandemonium struck the retail food system as a result of the coronavirus outbreak.

A widespread shut down of restaurants and a fear of future closures at retail has led to massive increases in retail sales. Confidentially, retailers have shared sales increases of 250%, 350% and more.

A part of that increase has been a boom in delivery. Walmart has been building its delivery mechanism for years. But, of course, Amazon.com is a competitor, and most grocery stores have some kind of online outlet.

Walmart’s strength is its ability to leverage its real estate footprint by offering “click-and-collect” options. Amazon sells a lot of grocery items through its established online service, but less through its dedicated food portals, such as AmazonFresh or Prime Pantry.

The coronavirus has probably led people to want to buy online. First, it lets them avoid other people and thus possible contamination. Second, many stores are out of stock on various items. So many consumers can buy from multiple vendors to meet their needs. Third, many stores are not themselves anymore. HEB, Wegmans Food Markets, Publix Super Markets and many others have all announced reduced hours of operations and the closure of in-store restaurants.

In future editions of this study, we will look to ascertain the degree to which online sales have come to compete with their brick-and-mortar cousins.

For now, the assumption is that in the not-too-distant future, we will see a return to normalcy. In store cafes will open. People will want to get out.

It is also true that things sometimes change forever. If consumers who never bought on line try it, some will find they like it. It also may be a long time before people are comfortable bumping into some random consumer on a check-out line.

Still, core values — Price, Quality, Assortment, Convenience — are bound to be important, and for the supply base it makes little difference, at least in the short term, if a supermarket sells the product by promising delivery, offering pickup or by having customers walk in the door.

COMPETITION WITH WALMART RELATIVELY NON-EXISTENT

If consumers do walk in the door of the seven separate supermarkets we visited for this study, when it comes to price they see something interesting. They see that, for the most part, supermarkets are unwilling or unable to compete with Walmart on price.

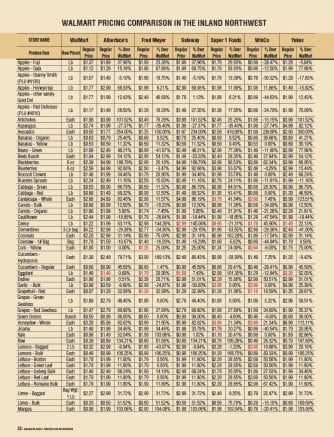

The two big semi-national chains, Safeway and Albertsons, don’t even seem to be trying! Safeway’s produce prices come up as 30.46% over those at Walmart, and Albertsons was 29.92% over Walmart. It is hard to believe that Safeway and Albertson’s have just decided to abandon the idea of being price competitive with Walmart, but that seems to be true – at least in produce.

Yoke’s Fresh Market comes in at the very top of the price comparison – showing its produce prices to be a full 35.02% over those of Walmart. Yoke’s fame is that it is an employee-owned company with 17 stores. Online you can find lots of praise for their produce. One Yelp reviewer wrote this: “Yoke’s consistently has the best quality produce and has some items that you can’t find at other stores around town, and the employees are always friendly and helpful.”

Still, is it really possible that the market will sustain a price so high compared to Walmart? For the moment, it seems so.

Super 1 Foods seems to be neither here nor there. Its produce is not as expensive as most of the retailers but not near the bottom, ranking 22.92% over Walmart.

Kroger’s Fred Meyer division, a concept not unlike the Walmart Supercenter, comes across as a bit not here and a bit not there in its pricing. It is a full 11.42% over Walmart, so it is beating most supermarket chains in produce pricing, but it is still letting Walmart beat it.

The big news out of this month’s review is the triumph of WinCo Foods. It beat Walmart, coming in with produce pricing 2.53% lower than Walmart. The mostly employee-owned company is aggressively growing, and its low price positioning is its calling card.

Interestingly enough, although WinCo wins our overall pricing measure, it really shows strength in our organic pricing comparison. There WinCo is 15.47% under Walmart. Fred Meyer comes in 4.75% over Walmart; 15.09% was the amount Yokes came in over Walmart on organics; Super 1 Foods came in at 19.94% over Walmart on the organic numbers; Safeway was 21.73% over Walmart on the organic assortment; and Albertsons was 23.75% over Walmart’s organic pricing.

Winco’s win in this category is partially reflected in a readjustment of the apple category to make sizes comparable.

Walmart is busy now, focusing on its online business. Maybe that will be enough. But losing its reputation as the low price leader won’t make its job easier.

Inland Northwest Price Survey Recap

The subject of this price check is an area known as the “Inland Northwest” or sometimes called the “Inland Empire of the Pacific Northwest”. This area constitutes the Eastern region of Washington state and northern Idaho. The primary cities in this area are Spokane and Spokane Valley in Washington, Coeur d’ Alene and Post Falls in Idaho.

Population in the region has been growing rapidly with a 14.5% increase in 2019, raising the region’s population to between 750,000 and 1 million. The influx of population is primarily been from neighboring states, especially large numbers of immigrants from California. The area contains a mix of national chains and regional operators competing in a fast-growing market. The following is a short description of the operators in this area:

Super 1 Foods: This is a local chain of warehouse-type stores affiliated with the Rosauers chain, owned by United Retail Merchants (URM), a local co-op. The stores were similar in structure and presentation to Cub stores in other areas of the country. The chain’s produce departments, however, are comparably smaller than the national chains and have less variety.

WinCo: This is an inter-mountain chain of over 125 stores throughout the Northwest and California. The chain is employee owned and has a complete warehouse format similar in many respects to Aldi and Lidl. The produce department is small, and all of the product is displayed in boxes on racks and the overall selection is basic with limited variety.

Yoke’s: Another employee-owned store, Yoke’s is a more upscale store offering many special departments and upscale merchandise. In produce, the department is a good size, and variety is above average; however, it doesn’t quite reach the scale of other upscale grocers across the country.

Fred Myers (Kroger): “Freddy’s”, as it is known in the area, is a member of the Kroger chain and is a very large store carrying a wide variety of merchandise, including jewelry, furniture, household goods, clothing, shoes as well as a complete grocery store. This operation is the market leader within the region and its produce departments are large with a wide variety of all items

Safeway: This is the second national chain within the area with several outlets spread across the region. A classic grocery store, these outlets have a wide variety of all grocery items and departments. In produce, there are large size departments with a wide selection of produce items both conventional and organic.

Albertsons: Another large national chain with several outlets in the region. Due to its merger with Safeway, Albertsons shares many of the aspects of presentation, advertising, and item selection. However, the produce departments tend to be smaller and have less variety than their Safeway counterparts.

Walmart: There are several large Walmart supercenters in the area, mostly newer types of outlets with expanded produce departments, utilizing individual displays, bins and tables to merchandise the product.

In comparing these outlets on price, we also reviewed the impressions and observations in several other areas of their produce operations. We will highlight six areas of operation and how the stores compare in each area.

Price: This was the major area of investigation in this area, and the results of the price checking was most interesting. There seems to be two distinct groups of stores in relation to their pricing. In the lower price area, WinCo seems to be the leader in terms of comparable pricing of items. However, Walmart may well be the low price leader when its wider variety of items is included. Super 1 Foods would be third in this group and just barely ahead of the second group.

The second group consists of middle-of-the-road pricing and is led by Fred Meyer, followed by Safeway and Albertsons. The most expensive in the second group would normally be in its own category similar to that of Whole Foods, but Yokes doesn’t quite qualify for the same category as Whole Foods and simply is the most expensive of the second group.

Variety and Selection: Once again there seems to be two distinct groups in this area of comparison. The best variety and selection group is headed by Fred Myers, followed by Safeway, Albertson’s, and Yokes. The second group is headed by Walmart, followed by Super 1 Foods and finally WinCo. The discrepancy between the two groups is obvious when one walks in the stores — abundant displays of a large variety of items around the department compared to the limited selections overall in the second group.

Presentation: The presentation comparison is similar in grouping to the other areas of operation mentioned, but we will compare them all in their appeal to the consumer of their overall presentation. This category is led by Fred Myers, followed by Safeway, Albertsons, Yokes, then a drop-off to Walmart and Super 1 Foods and then another drop-off to WinCo.

Quality and Condition: Overall quality and condition of the produce is good in all stores throughout the region. Because of this situation, the differences between each operation are smaller than in the other categories. At the top of the list are three companies — Fred Meyer, Safeway, and Albertsons. All three have excellent quality and showed proper rotation and maintenance of their displays.

Fred Myers earns a slight nod over Safeway, and Safeway has the same advantage over Albertsons. The overall quality and condition in the other four operators are a bit lower than the top three but are still good. Ranking this second group is difficult because they are so close; however, in my estimation they break in this order: Yokes, Super 1 Foods, Walmart, and WinCo.

Labor: Observations in this area reflect what I’ve seen throughout the country, where certain stores within chains take it upon themselves to increase their labor above what is dictated by management in order to serve their customers the best possible manner. The same is true in this area where the rankings for labor reflect commitments made to better serve the customers. The rankings are: Fred Meyer, followed by Yokes, Safeway, Walmart, WinCo, Albertsons, and Super 1 Foods. By standing in the produce department, you can see the additional workers building and maintaining the displays on a regular basis. As the rankings decline, the less personnel is seen working on the floor.

Organics: While there seems to be an increased emphasis on organic offerings in the region, some of the competitors have not yet fully embraced the need or the demand for organic produce. In this area, the larger national chains seem to show more inclination to stock a wide variety of organic items. This effort was led by Fred Myers and closely followed by Safeway.

The next group with good organic representation was headed by Walmart, followed by Albertsons. The final group had limited (at best) availability of organic, with the best of this group being Yokes followed by Super 1 Foods and bringing up the rear, WinCo.

In the case of WinCo’s organic pricing, it is in line with the store’s overall low-price approach.

- Limited overall selection and SKU’s: They do not carry many other organic items other than apples, so pricing has less pressure to produce revenue.

- Lack of volume: Because they feel they must carry some organic items, to avoid shrink from slow sales, they price aggressively, nearer to the conventional item price.

- Quality and Size: Given this is a non-objective area, this factor is based on several observations and visits. WinCo tends to sell smaller than the premium (larger) size apples the competitors use. Additionally, the overall quality and condition of the organic fruit is not as good as in the other stores. This is an old way to reduce cost and subsequently the price, which is often used in the conventional arena as well.

Given the minimum impact on overall revenue represented by its organic selection, such a pricing strategy on organic is sustainable at WinCo.

Going forward, the influx of consumers from other states, especially California, likely will help to drive the expansion of organics. It also should be noted that there is a single organic/natural store in each of these major cities in the area. The most promising looks to be Huckleberries (a new division of Rosauers) in the Spokane Metro area.

This completes the observations in various categories, and the identification of the strengths and weaknesses of the various players in this area. It must be noted that this is an increasingly dynamic area where all the players are constantly maneuvering to take advantage of the new influx of consumers into the area.

Historically this area has been slow to react to various trends across the country but has always been an area where price competition is been keen and maybe the reason that discount price competitors, such as ALDI and LIDL, have yet to make an appearance in the area. With the core growth rate being projected to maintain double-digits, this area will continue to grow and their cast of players may expand.

17 of 25 article in Produce Business April 2020

Have a story to share?

Take a place at Produce Business