Innovation Can Deliver Sales Growth

November 10, 2025 | 3 min to read

Smaller consumer packaged goods (CPG) manufacturers are innovating at scale to create “superstar” products, with average sales per innovation higher for small- and medium-sized brands than large ones. Tapping into local and sustainability claims and shoppers’ desire for products that excite, inspire and support their lifestyle, smaller challenger brands are highly effective in driving sales revenue through innovation — proving the old adage that “small is mighty.”

This conclusion is based on the Europe’s Innovation Pacesetters 2025 Report, published by Circana — a detailed study of over 75,000 new CPG product launches and renovations in 2024, encompassing food, drink, household, personal care, baby and pet products. The report analyzes point-of-sale data from Circana’s largest European markets, France, Germany, Italy, the Netherlands, Spain and the U.K. (EU6), and draws on consumer research to understand purchasing behavior.

Across Europe, ongoing geopolitical and economic uncertainty, coupled with inflation, has led to an overall decline in CPG innovation. The number of innovations fell by 20% compared to 2023, while sales of new products were down 17%. Only 5.2% of all CPG products were innovations last year, down from 6.2% the previous year; one of the lowest levels ever recorded by Circana.

The U.K. and the Netherlands had the highest inflation rates and suffered the biggest innovation declines in terms of value sales. The U.K. saw sales of innovations in edibles categories decline 28% between 2023 and 2024, while the Netherlands fell 43% over the same period.

Innovation is a proven source of growth and a way of delighting shoppers who are eager for new products at a time of cost-cutting and uncertainty.

Innovation is the lifeblood of CPG, a proven source of growth and a way of delighting shoppers who are eager for new products at a time of cost-cutting and uncertainty.

Despite New Product Development (NPD) declining year-on-year in all years since the pandemic, as companies focus on optimizing their portfolios and using shrinkflation to boost sales, there are significant pockets of growth among smaller and challenger brands and among some of our best-loved heritage brands reinventing themselves.

Circana’s analysis also reveals that new products perform better in their second year of launch as shoppers try them out, any distribution issues are sorted, and price adjustments are made.

Ananda Roy is senior vice president and industry adviser, Consumer Goods, Circana.

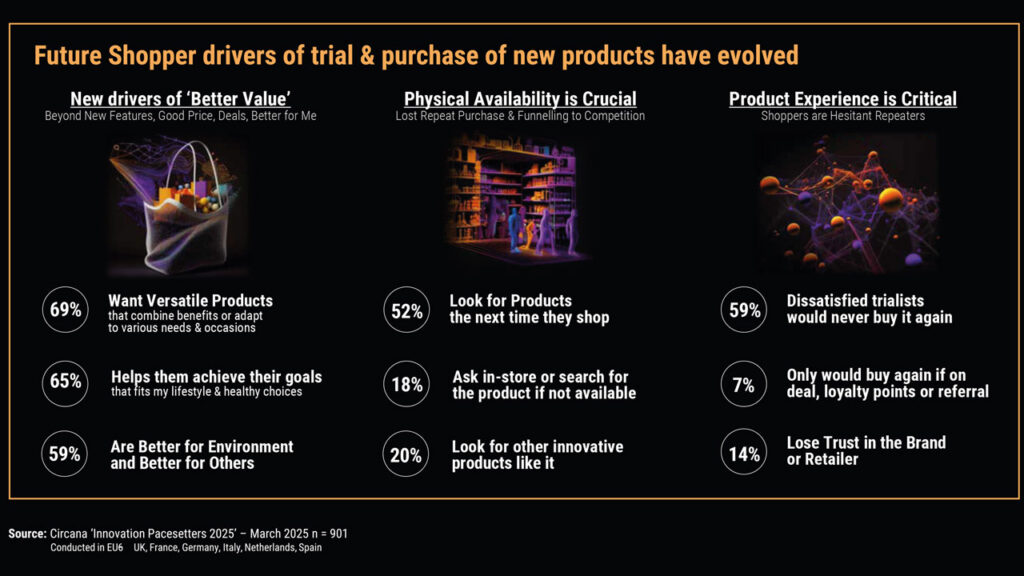

Circana analysed point of sale data for branded consumer packaged goods from the EU6: France, UK, Germany, Italy, Spain and the Netherlands, between Jan. 1 and Dec. 31, 2024. This was compared to trends in the previous full year 2023 and in some case studies to mid-term trends in 2021-2022. The report also draws on Circana’s Pacesetters Survey, undertaken in March 2025 with 1,000 consumers across the EU6, and Circana’s European Innovation Attitudes research, undertaken in April 2023 with 3,500 consumers in the EU6. Circana also uses proprietary analytical models to develop innovation rankings.

• • •

Fresh Category Under Pressure

- Innovation Value Share declined -1.5pp to 4.4% (FY2024 vs FY2023).

- Innovation in fresh, including fresh produce, struggled to maintain value growth.

- Innovation slowdown: Fresh is losing innovation share due to falling value and unit sales, despite being price sensitive.

- Small and niche fresh produce manufacturers are capturing afor premiumization and specialist positioning.

- Across EU6, demand for health-focused, functional, and convenient fresh formats is sustaining NPD success in selected subcategories like smoothies.

4 of 33 article in Produce Business October 2025

Have a story to share?

Take a place at Produce Business